Brazil – A review of the effects of inflation on the banking sector

Over the past 25 years, the Brazilian financial system has faced the challenge of functioning in an economic environment that became inflationary, hyperinflationary and subsequently returned to relatively stable prices.

The adaptation of the banking sector to these scenarios introduced peculiar characteristics that set the Brazilian financial services sector apart from that found in developing nations. These, and the economic changes that brought them about, are explored in this article.

Like most, the Brazilian financial system is based on two subsystems, regulatory and operating. In Brazil, they are integrated and interact effectively.

The bodies that make up the regulatory subsystem include the National Monetary Council, the Central Bank of Brazil, the Brazilian Securities Commission, the Superintendency for Private Insurance and the Secretariat for Complementary Pensions. These bodies of the Federal Government are responsible for formulating monetary policy, directing the functioning of the system within the macroeconomic guidelines and regulating the activities of institutions in the operating subsystem. These bodies are assisted in specific situations by others, which, while operating in nature, also take responsibility for specific regulatory guidelines, such as Banco do Brasil (farm credit), the National Bank for Economic and Social Development (long-term development) and the Federal Savings Bank (home financing).

The operating subsystem is made up of full-service (bancos múltiplos), commercial and investment banks, savings and loans, leasing companies, securities distributors and brokers, among others. The custody and settlement of almost all transactions in the banking sector are processed by specialised independent entities; and the agility and dependability with which transactions are processed in this operating subsystem deserves note. This environment was further enhanced after implementation in 2002 of the national Brazilian Payment System (SPB), resulting in the processing of settlements on a virtually real-time basis thus permitting better management of systemic risk in the financial system. Given the size of Brazil, in both geographic and population terms and the scale of technology applied, the new national payment system is remarkable.

Although the regulatory environment is complex, guidelines for the functioning of each of the regulatory units are well defined. Supervisory procedures and regulations have also improved, reflecting the strengthening of expertise locally, largely as a result of the application of best regulatory practices from abroad.

The beginnings of inflation

Inflation in the Brazilian economy veered out of control at the start of the 1980s. Inflation indices reached annual levels of nearly 100% and by the mid 1980s reached levels in excess of 200%. At the time, the economy did not benefit fully from mechanisms that were capable of reducing the risks inherent in such circumstances. Although these mechanisms (such as the application of monetary correction to transactions and the existence of a significant overnight market) already existed, they were not accessible by all bank customers, especially the less sophisticated.

The first consequences of adapting to this enviroment included a reduction in the provision of long-term credit by banks and the collapse of home financing, since the maturity of available funding was shorter than maturities typically required for home loans.

The Brazilian banking system was divided among four broad groups at the start of the 1980s: federally-owned banks, state-owned banks, private Brazilian-controlled banks and foreign- controlled banks. These groups each had separate and diverse interests and developed business strategies that were quite different from one another.

Federally-owned banks for the most part focused on developing and implementing specific credit policies such as farm credit, urban and regional development, among others. Banco do Brasil and Caixa Econômica Federal, both large federally-owned banks, developed extensive branch networks that competed directly with other retail banks and covered regions and customers that were not always of interest to private sector financial institutions. The administrative structures of these banks were not very efficient because employees received employment benefits only available in the public sector, such as tenured positions and differentiated retirement schemes.

State-owned banks also developed retail networks but these were mostly limited to their state of origin. They implemented credit policies that complemented the political interests of the governors of these states. Their administrative structures were generally similar to those of federally-owned banks.

Domestically-controlled private banks during this time comprised of two distinct groups. The first operated nationwide as part of a financial conglomerate with a large national branch network and with a broad range of products and services. The second operated in a more regional form and served a specific market niche.

Foreign-controlled banks had historically held a relatively small market share in the Brazilian financial market. For the most part, they were organised as representative offices of traditional international institutions that managed lines of financing offered to Brazilian companies, usually focusing on international trade finance. A select few had a retail presence; this was limited to large urban centres focusing on high net worth individuals, large local corporates and employees of international organisations’ global clients.

Hyperinflation and initial efforts to rationalise costs

In 1986, the implementation of a plan by the government (the Plano Cruzado) to halt the inflationary spiral then in course put the financial system and the economy as a whole to the test. The main objective of this economic plan was to reduce inflation by an artificial control of prices. The short period of relative stability during 1986, following its implementation, exposed the fragility of the financial system in an environment with controlled prices. This fragility was attributable to the adaptation of the system to the inflationary environment. Banks had become overly dependent on ‘float’ revenues, that is, the inflationary gains made on the distorted spreads between the interest and indexation on assets, and the cost of their non-indexed and non-interest or low interest bearing funds. This income grew to as much as 70% of the operating margins of banks during the inflationary period that preceded the Plano Cruzado. Without the gains, banks with excessive cost bases – there had been little pressure to control these, since the largest, remuneration of staff, had not been subject to the levels of indexation that banks’ assets had benefited from – had to restructure quickly. Two large banks became insolvent due to the loss of these inflationary gains and were subsequently liquidated by the government.

The hyperinflationary period that followed the Plano Cruzado from 1987 reduced the banks’ ability to generate direct float revenues as depositors were forced to protect themselves against constant daily inflation and manage their liquid funds more effectively by using instruments available in the overnight market. However, during this period, real interest rates and spreads increased (compensating the banks for loss of float revenues), which further focused banks’ activities on lending and deposit taking operations as an easy source of income.

It became evident that the system would face many problems in a stable economic environment given banks’ dependency on float revenues generated during periods of high and hyperinflation (see Figure 2).

One of the side-effects of the inflationary period is that the financial system was forced to, and had the resources available to, modernise by developing high quality technology-intensive processes. Brazilian banks have developed a reputation for their technological astuteness and many of them use integrated and real-time systems, especially in their retail and related treasury operations. Conversely, the exceptional float revenues also permitted the survival of institutions that had a scale of operations which was below their natural breakeven point and costs that exceeded accepted levels. As noted earlier, cost control had not been a major concern during the inflationary periods due to the distorted levels of float income.

One of the most significant steps towards rationalisation of costs in the Brazilian financial sector involved the implementation of the banco múltiplo or commercial bank concept in 1988. Before this, financial conglomerates were required to organise their activities in different financial areas using separate legal entities. The banco múltiplo concept allowed these different activities to be grouped in a single business entity, thus reducing operating costs.

The challenges of stability

It is only since the implementation of the Plano Real in 1994 that relative long- term stability has become a reality for the Brazilian economy. However, the structural problems of the financial system began to become evident after the Plano Real. Federal and state government-owned banks began to find it difficult to support their administrative structures. Banks, in general, began to face further challenges in maintaining earnings without the float income to offset the inefficient cost structures which had been ignored during the inflationary periods. Their scale of operations was insufficient and banks had not developed the practice of charging for services while the focus of attention was to attract deposits to generate float income. Furthermore, problems emerged within the credit portfolios as the corporate sector adapted to the lower inflation rates (see Figure 3).

Three programs were introduced to assist with the restructuring of the financial system:

(i) the Program to Stimulate the Restructuring and Strengthening of the National Financial System (PROER), designed to recapitalise private banks;

(ii) the Program to Stimulate the Reduction of the Banking Activities of State Governments (PROES), in order to clean up and subsequently privatise state-owned banks; and

(iii) the Program to Strengthen Federal Financial Institutions (PROEF) to clean up and recapitalisebanks controlled by the Federal Government.

These programs were considered to have produced satisfactory results in relation to their intended objectives and represented a relatively low cost to the tax payer when compared with similar programs implemented in other countries (see Figure 4).

PROER was implemented in the middle of a crisis provoked by the insolvency of three banks ranked among the ten largest private sector banks in Brazil. Simply liquidating these banks could have undermined confidence in the financial system. The monetary authorities intervened and immediately assigned the good operating assets and liabilities to other financial institutions, while continuing to manage those assets for which realisation was uncertain. In addition, a policy of early repayment of federal liabilities was adopted to inject additional liquidity into the system, thus maintaining its solvency.

The objective of PROES was not only to clean up state-owned banks but also to prepare them, when possible, for privatisation. In addition to having administrative costs that exceeded those of private sector institutions, these banks were also used by state governments to finance their debt and for other political purposes. Accordingly, loan delinquency ratios were higher than the average in the Brazilian market. The PROES stimulated the ‘federalisation’ of these banks, that is, majority ownership was transferred to the federal government. A process that included restructuring and recapitalisation was then initiated, ready for privatisation.

PROEF was instituted to clean up and capitalise the four main federally controlled banks: Banco do Brasil, Caixa Econômica Federal, Banco do Nordeste, and Banco da Amazônia. These banks held a significant volume of loans that were unlikely to be realised or for which returns were insufficient as a result of the development policies of the federal government. The approach in this case involved the transfer of these credits to the National Treasury, as well as the exchange of other non-liquid assets for ones with more liquidity and returns compatible with market levels.

Facing international crises

The Asian Crisis in 1997 presented another challenge for the Brazilian financial system. Immediately prior to the crisis, the domestic economy was being prepared for a gradual reduction in basic interest rates, while the banking system developed new service- related business strategies. Some private sector banks, especially those with smaller scale operations, began to borrow paying floating rates, while lending these same funds at fixed rates. However, the Asian Crisis resulted in local interest rates increasing significantly and unexpectedly. The Central Bank of Brazil acted by identifying institutions with problems and requiring action from shareholders or facilitating the transfer of control to the state before the situation worsened.

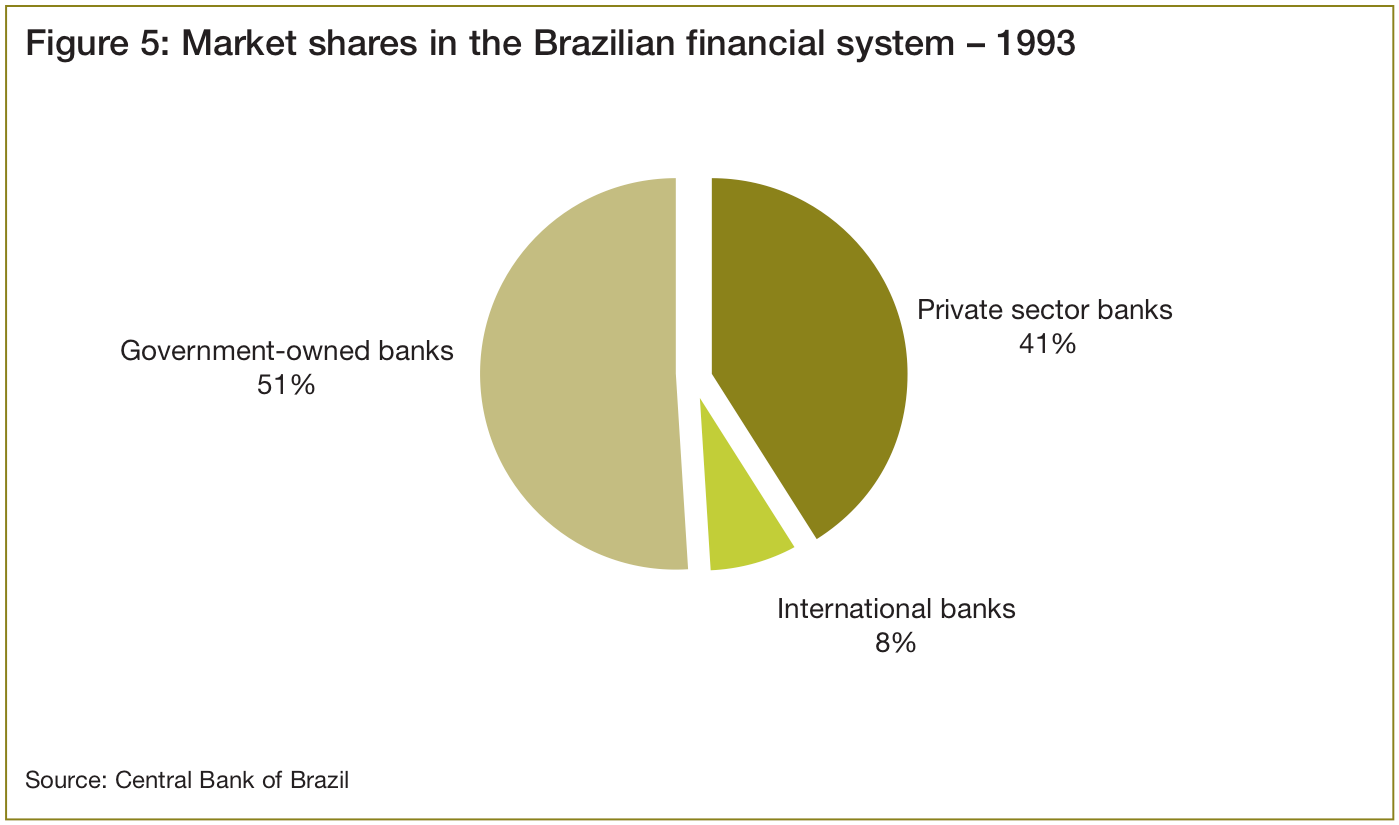

This facilitated the entry of new players – international banks – into the Brazilian banking system. These institutions, which had previously limited interests in Brazil, entered the Brazilian banking system by taking part in privatisation processes or acquiring medium-sized private sector banks caught up in the after-effects of the Asian crisis. Accordingly, of the eighteen largest deals involving acquisitions, associations or privatisations in the Brazilian banking market between 1997 and 2002, nine involved an international financial institution as buyer (see Figures 5 and 6 overleaf).

Brazil then faced the so-called ‘Brazilian Crisis’ during 1999. The practical

effect of this attack on its currency, the Real, resulted in its devaluation by approximately 70% during the month of January 1999. This did not, however, result in serious consequences for the banking sector, because many of the larger banks had anticipated the devaluation and entered into appropriate hedging arrangements. The Central Bank of Brazil provided the liquidity to the market while attempting to preserve the value of Brazil’s currency through intervention in the derivatives markets selling dollars. Only two small banks collapsed in this period as a result of the success of the initiative.

Consolidation and perspectives

The profile of the Brazilian banking sector is currently concentrated (the 20 largest banks hold approximately 80% of total assets in the system). The dominant banks include the two largest federally- owned banks and the three largest domestic private sector banks (which occupy the first five positions by assets) and five large international banks. In the short term, there is no expectation of significant change to this position.

Although the sector has become more concentrated, some institutions within the largest 20 have not yet acquired the scale of business necessary to achieve the sector’s average level of profitability. In addition, the macroeconomic environment still holds challenges that have yet to be dealt with by the sector. Brazil still has the second highest real interest rate in the world after Turkey. Lowering the basic interest rate is a particularly difficult challenge in Brazil, due to the fact that decreases in rates, while benefiting the government from a cost perspective, seriously increase the risk of hot money exiting the economy and downward pressure on the value of the Real. The Government’s economists have nevertheless indicated that interest rates should fall gradually over 2004. In fact, the Brazilian economy’s inter-bank interest rate has already fallen approximately 10 percentage points since July 2003 to its present level of 16.0% per annum. Furthermore, competition for banks and other lenders remains intense since, outside of the Government, there are relatively few corporates and other borrowers considered sound enough from a credit perspective and the consumer finance market is in its infancy (in relative terms). These factors point to a continued squeeze of bank spreads.

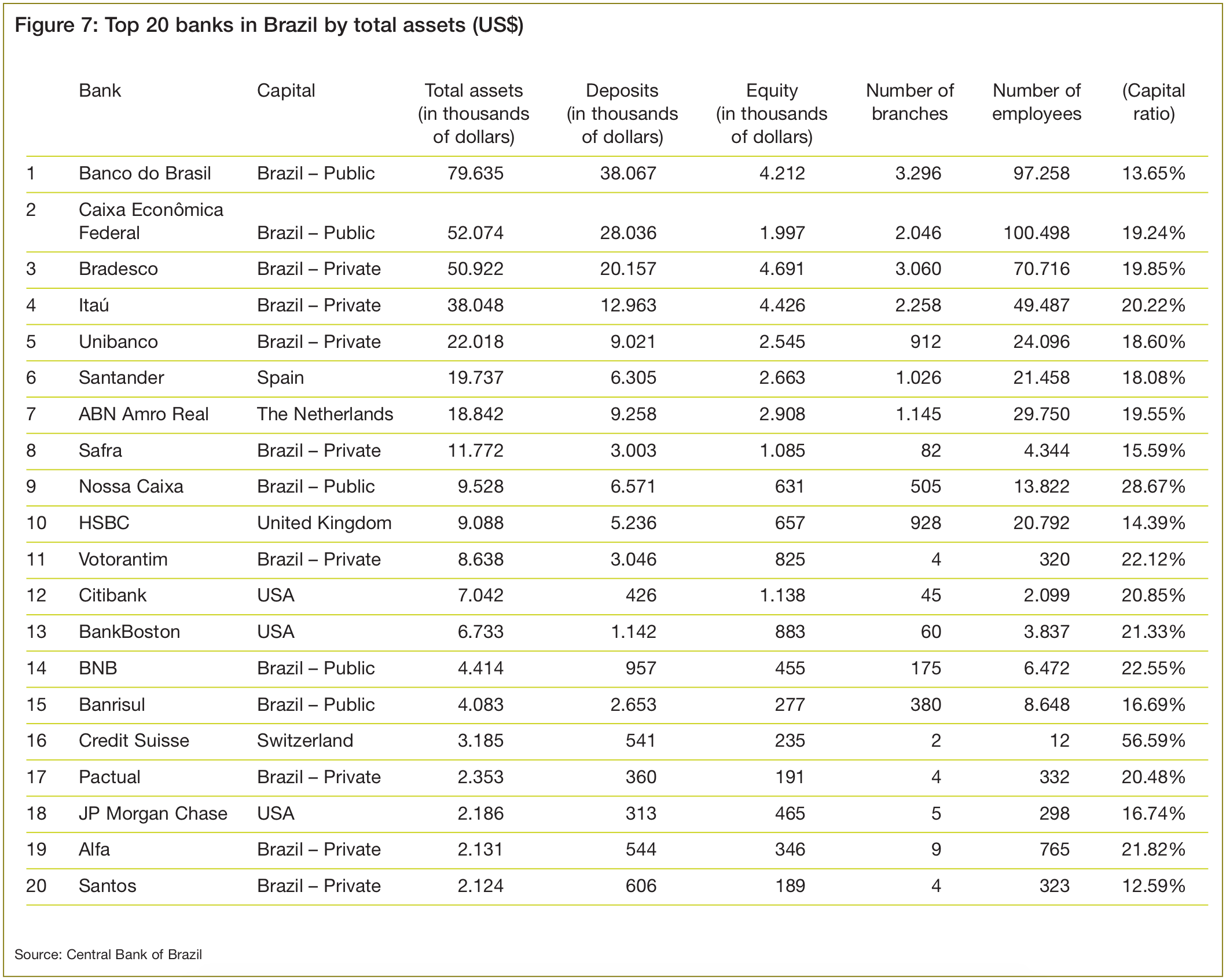

One of the alternatives for banks foreseen by the industry is the redirecting of funds that are presently invested in the money market, mainly in federal government securities, to corporate and consumer loan portfolios that provide higher returns. The share of loan portfolios in total financial assets in Brazil is still small (approximately 25% as of December 2003) and the capital ratios of Brazilian banks would allow this realignment (the average capital adequacy ratio of the 20 largest Brazilian banks is around 21% measured by reference to the Basel Accord (see Figure 7 overleaf)). Large banks have, therefore, begun to place more emphasis on their consumer loan businesses and the generation of commission business from services. This segment was previously served by smaller financial institutions. By focusing growth on their consumer loan business, the larger banks are also targeting the large number of individuals who have traditionally not done business with banks. Lower inflation rates have benefited the country’s huge segment of society which has operated in a cash- only economy: banks are now targeting this sector as the poor become more bankable and in their search for greater business volume and market share.

Ironically, the effects of the ‘inflationary’ years have resulted in the sector being technologically advanced but, by comparison internationally, narrower in the nature and breadth of banking services offered and from which revenues are generated.

The Brazilian financial system as currently structured has provided its participants with excellent returns. The average return on net income for the ten largest financial conglomerates was 23% in 2003. Economic stability, falling interest rates and consequent realigning of resources towards higher risk portfolios point to a potential reduction in these returns for the industry. This, in turn, will be offset as the overall market for bankable customers and the nature of both basic and sophisticated services offered by banks continues to grow.

Sergio Rogante, Paulo Miron e Graham Nye